Charles Bond, an Asian and Emerging Markets Equities Fund Manager, highlights a good example of a Chinese internet stock, Baidu, which has moved from being a contrarian investment to a very sought after stock.

In the latest Tenet Invest magazine, William Lam, Co-Head of the Asian and Emerging Market Equities team at Invesco, wrote about our contrarian investment approach in his article: I thought you said you were contrarian. We felt it relevant to supplement this with a comment on a recent stock example that has rapidly moved from being contrarian to popular.

At the time of writing, China’s leading provider of online search (Baidu), traded at about $125 per share.

Figure 1: Baidu share price at 30 September 2020

Source: Bloomberg, as at 30 September 2020

Baidu was a contrarian idea because the shares had fallen about 50% since 2018. Over this period the company had been struggling to grow their core search business due to competition for advertising spending from new apps such as Douyin (TikTok in China). At the same time, Baidu were making large losses in long-form video, as well as expanding into new unprofitable areas of artificial intelligence (AI), such as autonomous driving.

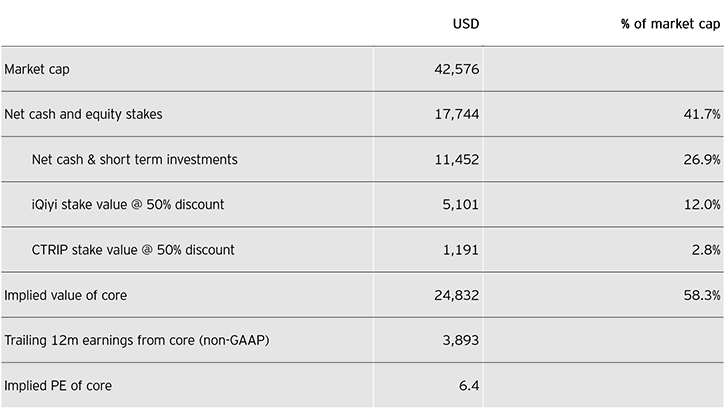

Given this backdrop and after excluding significant cash and investments, Mr Market was only willing to pay a single digit PE multiple for Baidu’s core business, and on our estimation assigned no value to the loss-making AI businesses. At the time, we commented that “this is the sort of multiple reserved for Chinese State Owned Enterprises (SOEs), businesses in steep decline, or where profitability is deemed unsustainable”. To us a 10-12X PE multiple for Baidu’s core business has always felt more appropriate given their market leading position and the potential growth opportunities.

Figure 2: Baidu’s sum of the parts valuation

Source: Invesco, as at 30 September 2020

Fast forward to today and Mr Market is taking a rather more optimistic view of Baidu’s prospects. Firstly, analysts now predict that Baidu will be able to grow its core search business as a result of Baidu successfully migrating traffic to its app from browser, as well as reduced competition and a broader recovery in China’s advertising market following the pandemic. UBS estimates that core revenue will experience a “double-digit growth recovery in 2021 and close to 10% beyond that”, and as a result are willing to ascribe a higher PE multiple to the business. Secondly, Baidu’s long-form video subsidiary (iQiyi - think Netflix of China) is now talking about breaking even by 2023 as a result of significantly reduced content spending, which will be additive to Baidu’s earnings. Thirdly, analysts are starting to get very excited about some of Baidu’s nascent AI businesses such as Apollo, its autonomous driving unit, which Mizuho estimate could be worth $40bn, roughly the entire market cap of Baidu as of 30 September 2020. As a result, shares in Baidu have risen rapidly to over $300 per share and sell side analysts are rapidly increasing their price targets.

Figure 3: Baidu share price today

Source: Bloomberg, as at 31 January 2021

To us, this example again reaffirms the strengths of a contrarian approach to investing - we like to buy shares in unpopular areas of the market because this is where we believe discounts to intrinsic value are most likely to be found. We don’t try to predict how and when the valuation anomaly is likely to be rectified, we simply believe that given the fullness of time, shares will trade at their intrinsic value.

Indeed, Baidu’s remarkable rise should act as a cautionary tale for analysts constantly on the lookout for “catalysts” to make Mr Market reappraise a company’s intrinsic value. To quote a sell-side analyst from the 17th of September 2020 when their price target was $130, “Any positive structural catalyst for Baidu - long promised, never delivered - remains too uncertain to forecast, while its execution track record is clearly poor”. To us this entirely misses the point and we would point to a quote from Anthony Bolton that explains why; “in my experience it’s very unusual to see a significant [valuation] anomaly and at the same time the catalyst that will correct it - if it was that obvious the anomaly wouldn’t be there in the first place”; we wholeheartedly agree.

Find out more

For more information about the Invesco Asian Fund (UK) and the contrarian investment approach that it employs, visit invesco.co.uk/asianfund.

Investment risks

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested.

The fund invests in emerging and developing markets, where there is potential for a decrease in market liquidity, which may mean that it is not easy to buy or sell securities. There may also be difficulties in dealing and settlement, and custody problems could arise.

The Fund may use Stock Connect to access China A Shares traded in mainland China. This may result in additional liquidity risk and operational risks including settlement and default risks, regulatory risk and system failure risk.

The fund may use derivatives (complex instruments) in an attempt to reduce the overall risk of its investments, reduce the costs of investing and/or generate additional capital or income, although this may not be achieved. The use of such complex instruments may result in greater fluctuations of the value of the fund. The Manager, however, will ensure that the use of derivatives within the fund does not materially alter the overall risk profile of the fund.

Important information

This article is for UK Professional Clients only and is not for consumer use.

All data is as at 31/01/21 and sourced from Invesco unless otherwise stated.

Where individuals or the business have expressed opinions, they are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice.

This article is marketing material and is not intended as a recommendation to invest in any particular asset class, security or strategy. Regulatory requirements that require impartiality of investment/investment strategy recommendations are therefore not applicable nor are any prohibitions to trade before publication. The information provided is for illustrative purposes only, it should not be relied upon as recommendations to buy or sell securities.

For the most up to date information on our funds, please refer to the relevant fund and share class-specific Key Investor Information Documents, the Supplementary Information Document, the Annual or Interim Reports and the Prospectus, which are available using the contact details shown.

Issued by Invesco Fund Managers Limited, Perpetual Park, Perpetual Park Drive, Henley-on-Thames, Oxfordshire RG9 1HH, UK. Authorised and regulated by the Financial Conduct Authority.